African countries are systematically losing their taxing rights over cross-border services due to significant restrictions in tax treaties. This has been evidenced by several tax treaty disputes in Kenya. These treaties (double taxation agreements) are designed to prevent double taxation or double non-taxation by allocating taxing rights between two countries.

These disputes expose a deep structural problem: despite the fact that a significant volume of services are imported by Kenya, unless they are attributed to a service provider’s fixed place of business, Kenya cannot tax the income arising from such services. This is not just a Kenyan issue, but a continental issue.

African countries significantly import services. According to the World Trade Organisation, in 2024, Africa imported 36.3% and 42.5% of its professional and management consulting services from Asia and Europe, respectively. In the same year, it imported 25.6% and 50.7% of technical, trade-related, and other business services from Asia and Europe, respectively, whilst intra-African imports accounted for only 3.1%.

Considering this data, it is clear that Africa cannot continue importing services while exporting its taxing rights and that something must be done to safeguard these taxing rights. This blog seeks to explore this structural problem by delving into two Kenyan cases on the taxation of cross-border services.

Significance of technical, managerial and professional services

Kenya is a net importer of professional, managerial and consulting services. In 2024, the highest value of these imports amounted to around 207 million US dollars from one trade partner. Meanwhile, the highest value of exports in professional, managerial and consulting services Kenya was to the United Kingdom, amounting to only around 33 million US dollars.

On the other hand, Kenya imported the highest volume and value of technical, trade related and other business services from the US amounting to around 194 million US dollars while exporting only around 61 million US dollars to the UK.

Data from 2024 further shows that Kenya imports most of its commercial services, including technical services, from the United States, the United Kingdom, China, India, Ireland, the Netherlands, France, and Singapore. In totality, this data shows that Kenya is experiencing a services resolution, similar to what is happening within the rest of the continent. However, this revolution is characterised by an increase in the share of gross domestic product attributable to services, a decline of export of services by developing countries and high-income countries dominating exports.

This means that invariably, Kenya like many other African countries, is a source country within the context of taxation of cross-border services. As a source country, Kenya must be invested in ensuring that income derived from these services is taxed in Kenya rather than taxation in the residence country (i.e. where the exporters of said services are based). Yet despite this, there are significant gaps in Kenya’s framework for taxation of services as evidenced by the cases of Commissioner of Domestic Taxes v Total Kenya Limited [2024] and the case of Commissioner of Legal Services and Board Coordination v McKinsey and Company Inc. Africa Proprietary Limited [2026].

The McKinsey and Total case: Kenya’s approach to taxation of services

As per Kenya’s domestic laws, income derived from the payment of management or professional fees for services rendered would attract a withholding tax of 20%. Management or professional fees are described by Kenya’s income laws as ‘a payment made to a person, other than a payment made to an employee by his employer, as consideration for managerial, technical, agency, contractual, professional or consultancy services…’ However, these provisions are constrained depending on the existence of double taxation agreements. This means the rate of 20% will no longer apply. Instead, two things may happen:

- Kenya will tax the income derived from these services at its corporate tax rate, meaning such income shall be treated as business profits. This income shall be taxed as business profits only when it is proven that these services were being provided through a fixed place of business by the service provider within Kenya.

- Kenya taxes the income from these services at a reduced withholding tax rate e.g. 10%.

Scenario 1: Fixed place of business

The scenario described above will mean that Kenya’s taxing rights are triggered only when a permanent establishment (PE) is said to exist. For a PE to exist, the following conditions must be met: the place of business must be fixed; and the carrying on of the business of the enterprise must be through this fixed place of business. This rule was established when services had to be physically performed by the service provider within the source country.

This is no longer the case with the advent of digitalisation and globalisation. It is possible for such services to be provided wholly or partially remotely. Realising these changes, many DTAs provided for a ‘services’ permanent establishments. This means that a place where the furnishing of services is carried out can be considered a PE as long as certain temporal conditions (e.g. 183 days within a 12 month period) are met. Even with the services PE, a certain level of physical presence is still required thus, only partially eliminating the problem. Nevertheless, many Kenyan DTAs that are currently in force, do not have this provision and thus we fall into the first category whereby physical presence in the form of a fixed place of business must be proved.

The difficulties of proving the existence of a PE are well demonstrated in the McKinsey case. In this case, the service provider was a South African entity known as McKinsey South Africa Pty Ltd. (McKinsey South Africa). The Kenya Revenue Authority (KRA) was demanding withholding taxes from the professional fees that had been paid by the Kenyan taxpayer, McKinsey and Company Inc Africa Proprietary Ltd (McKinsey Kenya) to the service provider for consulting services.

The Kenyan taxpayer argued before the court that firstly, any income arising from the payment of professional fees should be treated as business profits in accordance with the Kenya – South Africa DTA. Thus, it was necessary to prove that a permanent establishment existed. Secondly, they argued that the service provider did not have a permanent establishment in Kenya since they were not a branch of McKinsey South Africa but rather they were a subsidiary of another South African entity that was not the service provider. Unfortunately, due to the failure to prove that there was a PE in Kenya, the taxing rights over this income were then allocated to South Africa.

Scenario 2: Reduced withholding tax rate

DTAs will allow source countries to tax income from services such as professional, managerial, and technical services as long as there is a specific article therein specifying the tax treatment of these services. Additionally, these articles also provide a lower withholding tax rate (often 10%). These articles are critical that they allow source jurisdictions to be able to tax technical services even in the absence of physical presence.

The absence/ presence of this article reflects a deliberate policy choice that mirrors the different interests of service-importing and service-exporting countries. Under the OECD Model Tax Convention (MTC), technical services are typically treated as business profits, meaning they are taxable only in the service provider's residence state unless attributable to a permanent establishment (PE) in the source state.

This is not surprising since the OECD MTC is often used by service/ capital exporting jurisdictions. The challenges and complexities arising from this scenario have been illustrated above and have been evident for decades. Some authors highlight that “technical fees are often payments that refer to the hiring of skilled technicians or consultants. The technicians or consultants involved will then perform their work in the source country, the country of the client. Their presence in the source country usually does not constitute a PE.”

By contrast, the UN MTC recognises the need for source-based taxation of technical services. The UN MTC has been amended to align most with developing countries that are net importers of capital, services and technology. It is only right that with changes as a result of digitalisation and globalisation of services.

In 2017, the UN introduced Article 12A to allow the taxation of fees for technical services, even in the absence of physical presence. Accordingly, a country has the right to levy a withholding tax on fees for technical services if the payer is a resident of that country or a non-resident with a permanent establishment. Prior to this, income from services was taxable either as business profits or if the services were independent, personal services provided by an individual through a fixed base in the source State.

Article 12A has since been replaced by Article 12AA, which gives the source of jurisdiction the right to charge a gross withholding tax on payments for services arising in the country, with the rate to be agreed upon during bilateral treaty negotiations. The new article has broad application to all types of services beyond technical services.

The stark difference between the two models lies in the extent to which they allocate taxing rights to source jurisdictions in the absence of a permanent establishment or fixed base, with the OECD model being skewed in favour of residence jurisdictions, which are mostly global north countries.

Overview of Kenya’s Double Taxation Agreements

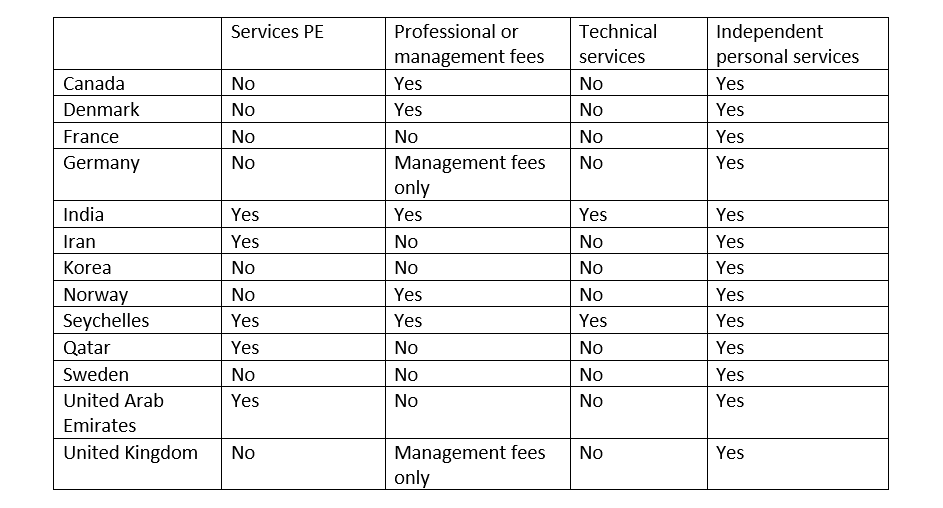

Having examined the 2 scenarios above, a question arises: How do Kenya’s DTAs treat cross-border services?

The table below shows that a vast majority of Kenya’s treaties that are in force do not have any clause on technical fees. The bulk of these treaties would thus require that physical presence be proved so that Kenya’s taxing rights can apply. These treaty restrictions are estimated to have cost Kenya around USD1.148m over 17 years.

Scenario 3: The ‘other income’ clause

The previous section has shown that unfortunately many DTAs in existence do not have a ‘technical services’ clause. Kenyan tax administrators are aware of this challenge, which is why in many instances, they rely on the ‘other income’ clause within these DTAs.

The decision in Commissioner of Domestic Taxes v Total Kenya Limited [2024], illustrates how this scenario often plays out and the consequences of treaty silence on fees for technical services. The court held that Kenya could not tax fees for technical services because such rights were not explicitly allocated in the DTA. It held that “...in the event Kenya wished to allocate itself taxing rights in the present DTA nothing would have been easier than for it to make express provision for the same by including articles similar to Article 12 A or Article 5(3)(b), as it has done in the past, with several other countries.”

The question before the court was whether professional fees paid by Total Kenya Limited to its holding company TOM, headquartered in France, was subject to WHT. The Commissioner argued that Kenya had the right to impose WHT on technical fees paid to a French non-resident without a permanent establishment. It argued that the technical fees were within the category of “other income” under Article 21(4) of the Kenya-France DTA, and therefore, subject to WHT pursuant to section 35 (1) (a) of the Income Tax Act (ITA).

The taxpayer argued that the technical fees were taxable in France as business profits. The Kenya-France DTA does not include an Article 12 on the taxation of technical fees. Income that is not addressed by any other article within DTAs often falls under the ‘other income’ clause. However, the High Court in the Total and the McKinsey case, has asserted that payment for such services would not fall under other income because it falls within the ambit of article 7 which address business profits.

Addressing the taxation of cross-border services through the UN Tax Convention

The emerging United Nations Framework Convention on International Tax Cooperation provides an opportunity to rebalance taxing rights with regard to services, which were eroded by DTAs. Article 5 of the current draft of the framework convention places an obligation on member states to renegotiate bilateral tax agreements to ensure the fair allocation of taxing rights beyond the nexus rules of value creation, economic activity, and revenue generation.

The Africa Group proposal is in support of the renegotiation of bilateral agreements with the proposal specifically providing that “State Parties shall, amongst others, adopt measures to enhance fair allocation of taxing rights, including through;…e) interpretation, application, and, where necessary, renegotiation of existing tax treaties and related agreements to ensure consistency with the principles set out in this Article.”

Additionally, the Africa Group has continuously proposed that, in defense of source taxation rights in services, the physical presence of rule should be reviewed and eliminated with regard to certain services.

The agenda for reforming the global tax architecture should be understood in the context of the ongoing services revolution. Modern services linked to ICT have been accelerating due to greater tradability, advanced technology, and lower costs. As a result, the taxation of services under DTAs has been a contentious issue resulting from the exclusion of an article on fees for technical services. The question confronting the international tax community is what the relationship between the Framework Convention and bilateral tax treaties in force should be, and whether the Framework Convention can serve as a fast-track mechanism for amending bilateral tax treaties?

Developing countries are most affected by treaty networks and lack the bargaining power or administrative capacity to negotiate fair terms, resulting in lopsided agreements despite the changing fiscal landscape, especially on services. The Framework Convention should have a role in the renegotiation or amendment of bilateral tax treaties. African countries should have withholding taxes on fees for technical services, include Article 12A in DTAs, and support the renegotiation or amendment of tax treaties through the Framework Convention.

Where technical services are provided by an enterprise of one Contracting State to an associated enterprise in the other Contracting State, there is the possibility that the payments may be more or less than the arm’s length of price of the services. Within a multinational group, fees for technical services may sometimes be used to shift profits from a profitable group company resident operating in one country to another group company resident in a low-tax country. Also, the revenue-generating potential from taxing technical services most affects developing countries, as they are importers of technical services and, in most cases, lack the administrative capacity to control or limit base erosion and profit shifting through anti-avoidance rules in domestic law and tax treaties.

Tax Justice Network Africa (TJNA) estimates that, in total, the world is losing over $483 billion a year to corporate tax evasion by MNEs, including through unfair tax treaty networks. The loss from DTAs that have outdated permanent establishment rules, encourage treaty shopping, round tripping and limitation of treaty benefits is substantial in the millions. In Uganda, TJNAs 2018 research estimates that Uganda’s revenue foregone under its tax treaty with the Netherlands was between US$8 million and US$24 million.

In conclusion, Kenya’s treaty practice highlights a broader structural imbalance in international tax law. Without explicit provisions allocating taxing rights over technical services, source countries will continue to lose revenue in an increasingly digital and service-driven global economy. The adoption and consistent inclusion of Article 12A are not merely technical adjustments; they are necessary steps toward restoring fiscal sovereignty for developing countries. If Africa is to truly tax value where it is created or where real economic activity takes place, then technical services must no longer remain in the blind spot of international tax rules.

Africa must dare to invent the future in which the fair allocation of taxing rights for services is non-negotiable. African countries need to renegotiate unfair tax treaties, adopt Article 12AA, insist on lower PE thresholds, strengthen anti-abuse provisions in DTAs and align treaty policy with the UN Framework Convention.

This blog was co-authored by Dr. Zandile Ndebele and Everlyn Kavenge Muendo of Tax Justice Network Africa.

For more information, please contact Everlyn Muendo at emuendo[@]taxjusticeafrica.net.